The Opportunity

A Canvas for Visionary Development

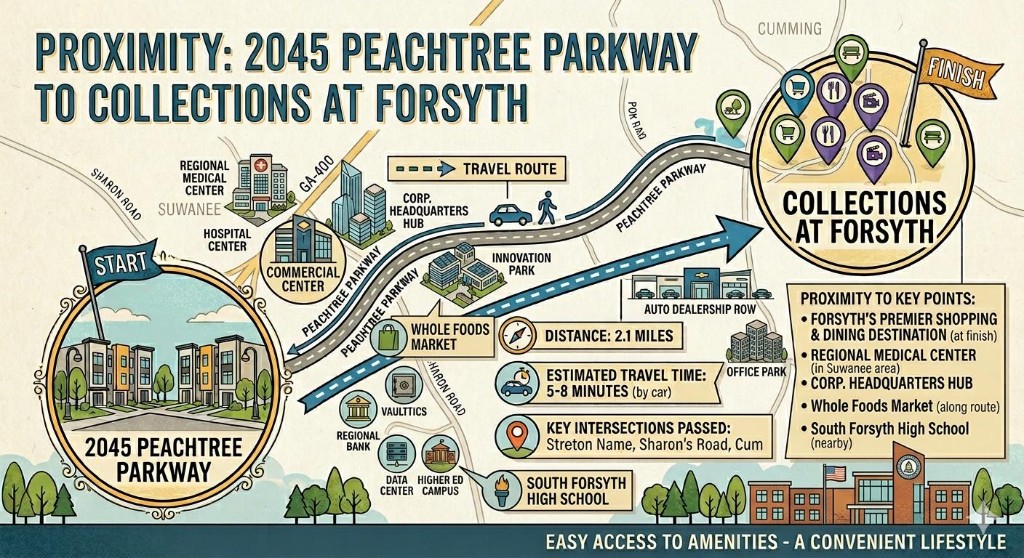

18.5 acres of prime real estate at 2045 Peachtree Pkwy in Cumming, Georgia — at the corner of Bagley Road and GA-141 (Peachtree Parkway) — positioned at the heart of one of Atlanta Metro's fastest-growing counties. This is a rare chance to shape the next landmark of Forsyth County's booming commercial corridor.

The development plan calls for 170,000 square feet of leasable space across a thoughtfully designed mixed-use campus, with 630 dedicated parking spaces ensuring seamless access for tenants and visitors alike.

With exceptional GA-141 frontage, one of the fastest-growing demographic profiles in the Southeast, and surging retail and office demand, Peachtree Corridor represents a generational investment opportunity.